One word can totally collapse your world as you know it. It can destroy your financial stability and cause a negative spiral in all aspects of your life. Business owners worry about how their bad business may affect their personal finances. Could they lose their home, or will their life’s savings be wiped out? This is why this one word can cause so many anxious emotions in people. The best way to alleviate this anxiety is to avoid getting into any situation involving a discussion about bankruptcy.

Your business is not only the way you earn income, but it also defines you. You want to be proud of its success and ensure stability for yourself, your family, and your employees. In 2022, over 13,000 businesses declared bankruptcy in the United States. The bankruptcy number has fallen since the 1980s and reached a historic low in 2022. That is a positive trend, but many businesses and families continue to be impacted by something that could easily be prevented. How does a business end up in bankruptcy? What could be done to avoid this from occurring? Here are some things to consider for your business to avoid having to utter those nightmarish syllables.

No Rainy Day Planning

Even the most insightful business planner cannot predict every possible potential threat to their plan. Things will come up that you simply cannot see (like a worldwide pandemic!) However, putting contingency plans together for low sales periods or other market disruptions is essential for your business. This is often overlooked when a new business is starting since the basic operations are at the forefront. Any financial advisor or accounting expert will tell you that you must save for a rainy day because it is highly likely that day will eventually come. Every business should have and maintain a rainy day fund and plan that can be implemented if something like a pandemic, medical issue, family issue, etc., should occur. Your rainy day fund may be a big bucket of cash that can be used when needed to supplement your income or a plan that includes laying employees off for a short period. Regardless of what it is, having that contingency in place will help you to avoid bankruptcy if something should go wrong.

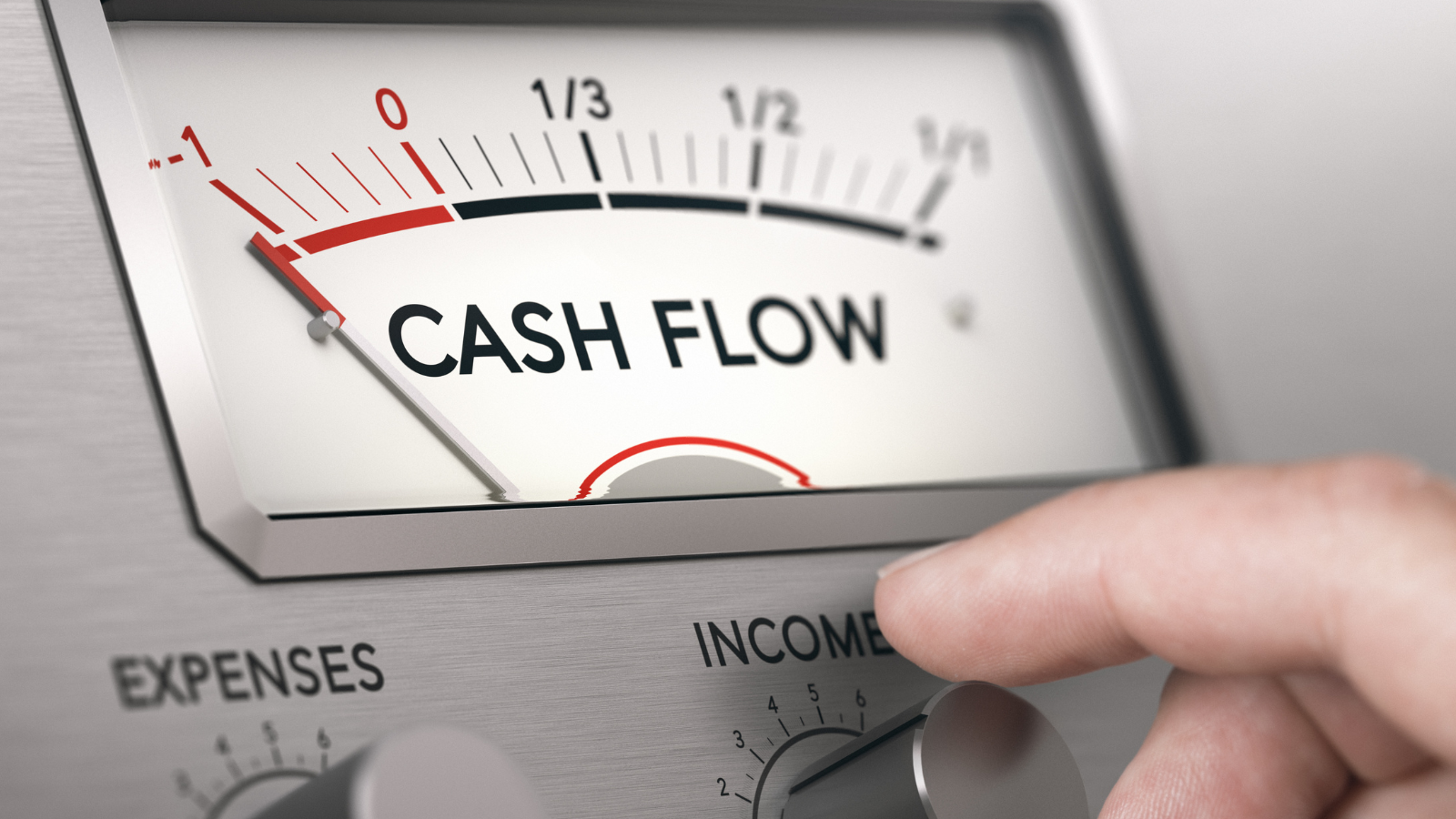

Cash Flow Problems

Calculating the cash flow of your business can be challenging, even for the experts. Many variables can impact the money coming into your business. Since many small business owners are a little “loosey-goosey” about how they bill their clients and collect the money, cash flow can quickly become a huge problem. When the money does not come in fast enough to cover your costs, bills pile up, vendors blast your email inbox, and your employees threaten to quit. These scenarios may cause the thought of bankruptcy to enter your mind.

You can avoid cash flow problems through good planning and even better procedures. As a business owner, you always want to do the right thing for your clients/customers. This does not mean you have to give something away for free (like your time) or let them draw out paying you. Hire a good bookkeeper or accounts manager to help you with this process. Include things like these to keep your business flush with cash.

- Develop a standard contract for any of your products or services.

- Make certain contracts are signed before you begin a job or sell the product.

- Invoices should clearly be labeled with expected payment terms.

- Accounts Receivable should be worked regularly with follow-up calls as needed.

- If someone does not pay, hire a collection agency to help you get the money.

Your business should be a fun and rewarding endeavor. Putting this one fundamental process in place will keep it that way. It could literally mean continuing to be proud of what your business is doing or closing up shop and filing for bankruptcy.

Circumstances Change

Change is inevitable in life. From small changes to mega changes, your business will also be impacted. Essential employees will likely leave you at some point. Competitors will enter the market you once cornered. Giant customers who once loved you may find another vendor. How you weather these changes will determine if your business continues to succeed. Your contingency plans will help you adjust by hiring new people or finding an even bigger customer to replace the one you lost. It will require work and attention on your part. Without your leadership at the helm, even the best made plans will fail. Business owners must constantly adapt and change. These constant changes are what will keep you engaged with your business and out of bankruptcy.

Always continue evaluating your business. You may have a service or product that reaches many people. You could have a niche market that corners a segment of people. Either way, regular check-ins with your internal processes and the market segment are vital to avoiding the dreaded word bankruptcy.

Having an expert CPA firm will help keep you on schedule. They will work with you to ensure your cash flow is on track, your tax liabilities are known, and bankruptcy is avoided. The Hayes & Associates CPA team is available to keep your business on the right track. Contact us today to begin an evaluation.